China GDP rose 18% in Q1 2021.

U.S. GDP estimates were higher.

It is a very good time to invest in commodities as they are all breaking out. To do this, buy the holy trinity: VALE, SBSW, CSFFF.

China GDP rose 18% in Q1 2021.

U.S. GDP estimates were higher.

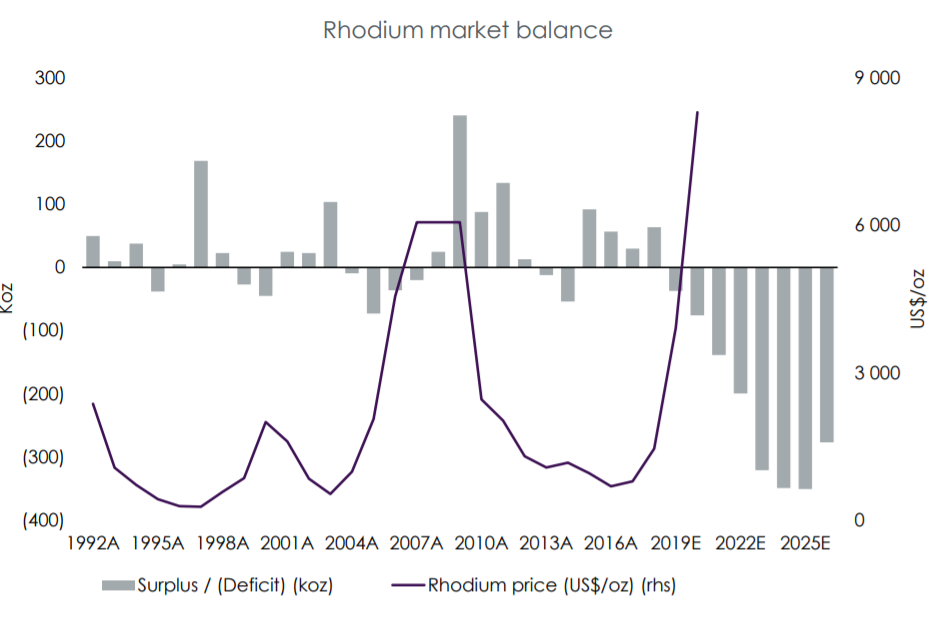

The CEO of Sibanye Stillwater got really uncomfortable about the rhodium supply in the last 5 minutes of this conference call, mentioning confidentiality on rhodium supply and its partners.

When being asked about rhodium supply, the CEO responded:

Neil Froneman: \”You ask some questions that would be confidential that we may not be able to answer them…\”. \”The rhodium supply decline is not going to come from us but from other producers and that would exacerbate demand. I would prefer we wouldn\’t answer your question about rhodium because it\’s market and relationship sensitive. I prefer we wouldn\’t answer it on this call.\”

I expect rhodium to moon shortly.

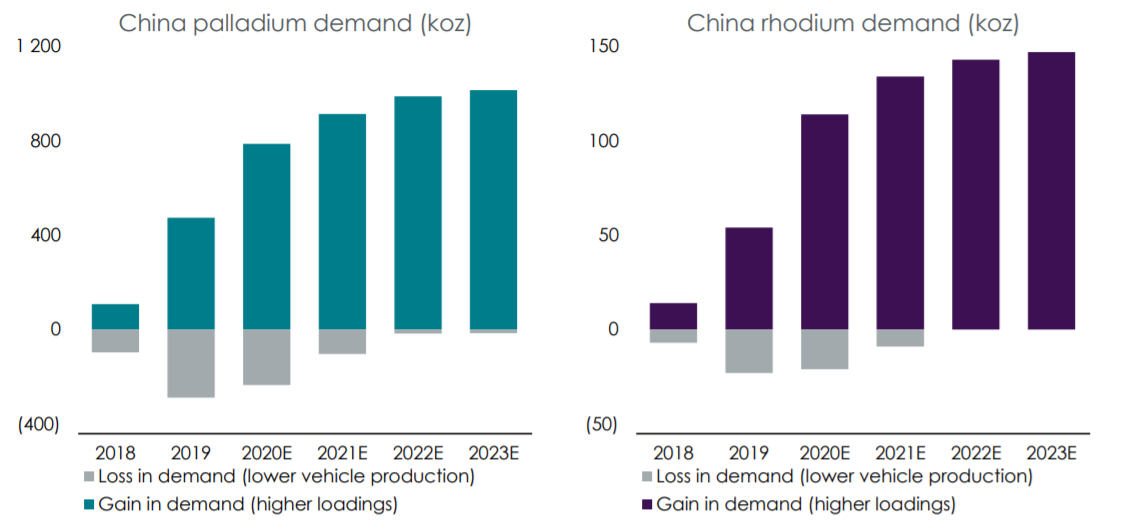

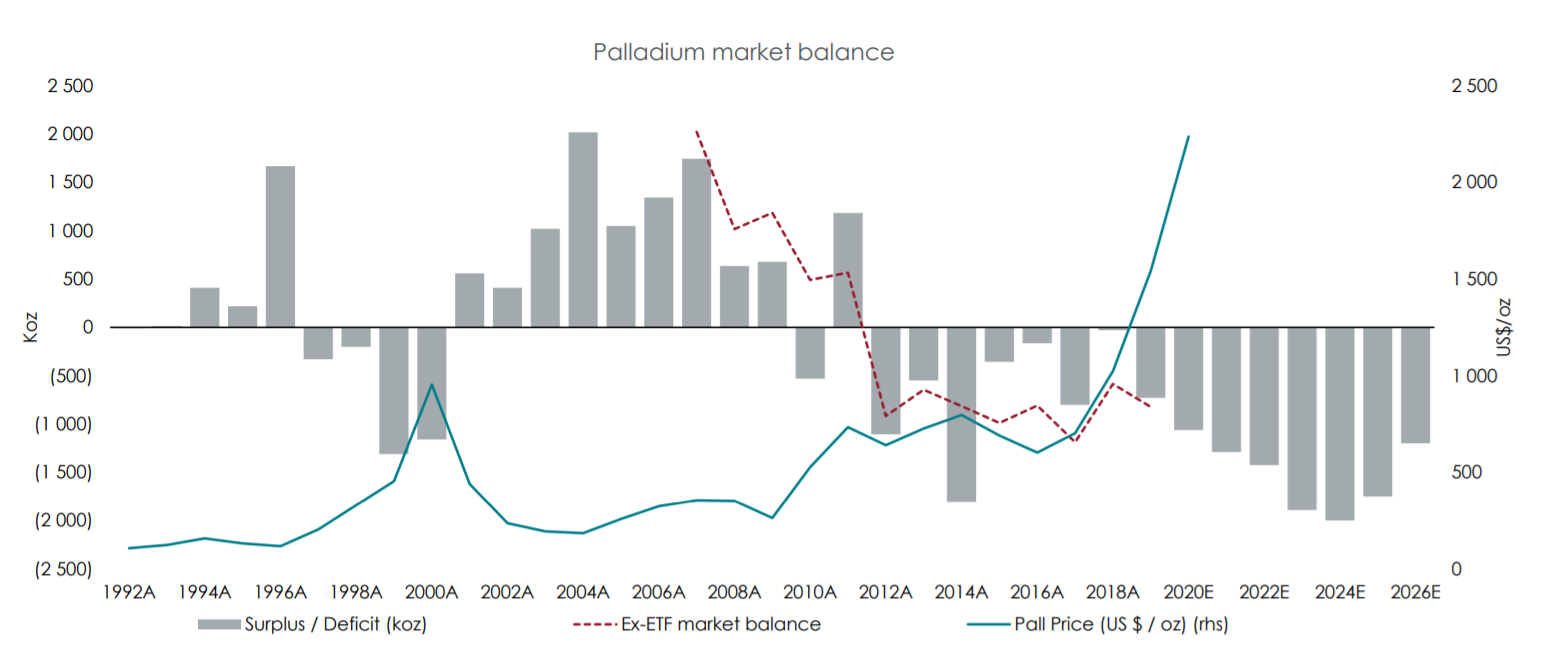

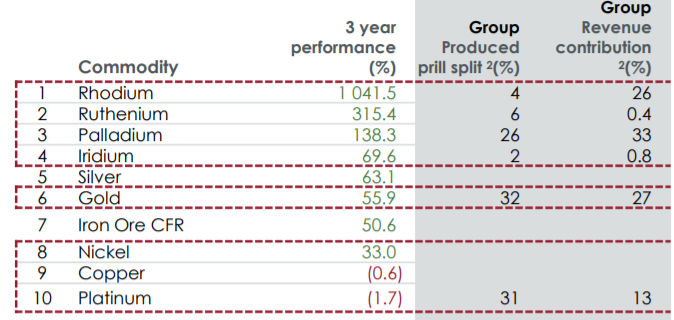

Platinum, palladium and rhodium have all been moving higher and I expect them to go higher as China is loading more palladium and rhodium in their vehicles. China vehicle sales have rebounded as well.

Platinum is going to be used in 3-way catalysts, which will boost platinum prices. Sibanye-Stillwater expects platinum to reach $2000 per ounce in 2025.

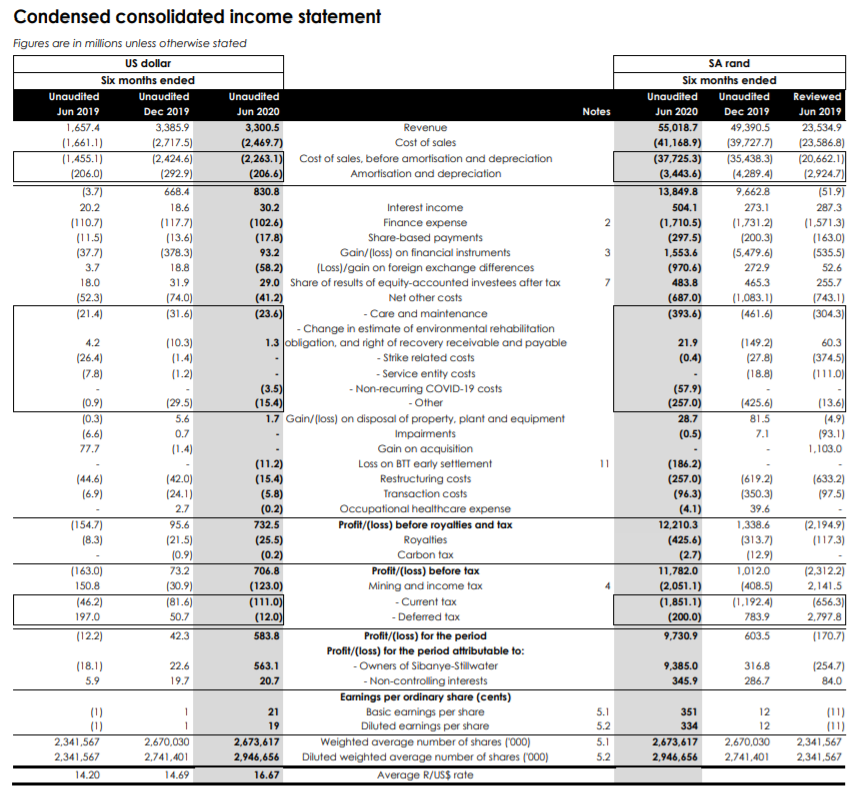

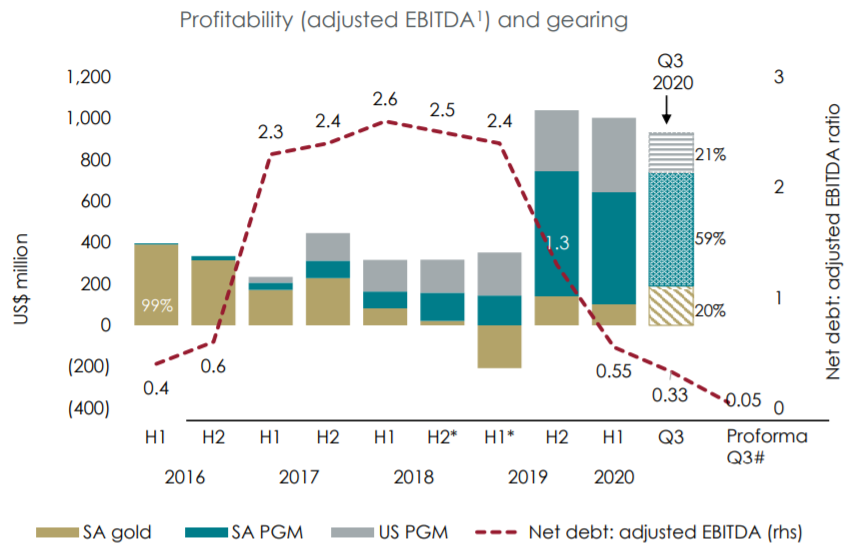

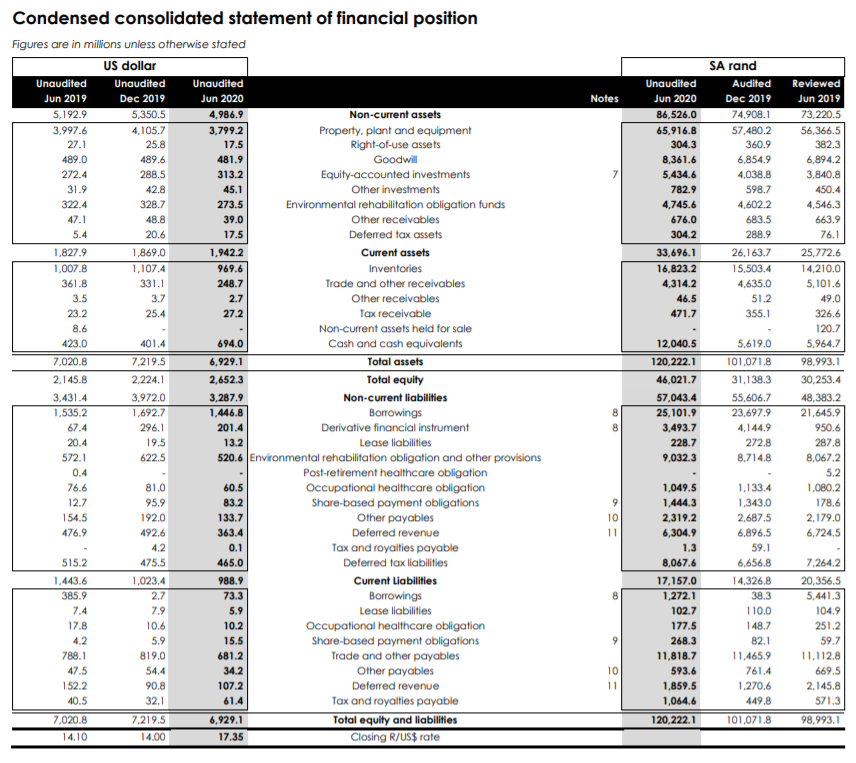

SBSW’s EBITDA was $922 million in Q3 2020. This translates to $3.7 billion EBITDA per year. With a 5 multiple, SBSW should be valued at $18 billion market cap. So there is 50% upside. The company has no net debt.

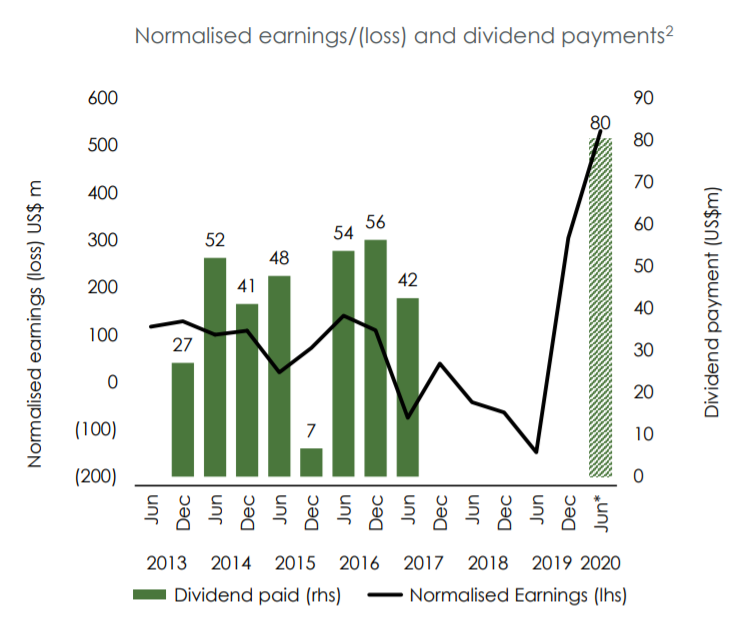

Net earnings were $1 billion per year in 2020, but is expected to rise 66% on higher rhodium/platinum prices and higher production numbers. Earnings per share are expected to be at $3.52 per share, which gives Sibanye-Stillwater a P/E of 4.8 which is very cheap.

On top of this, SBSW is expected to offer a dividend yield of 8% and is also moving into the battery metal space.

But price to earnings ratio is ok at 5-7.