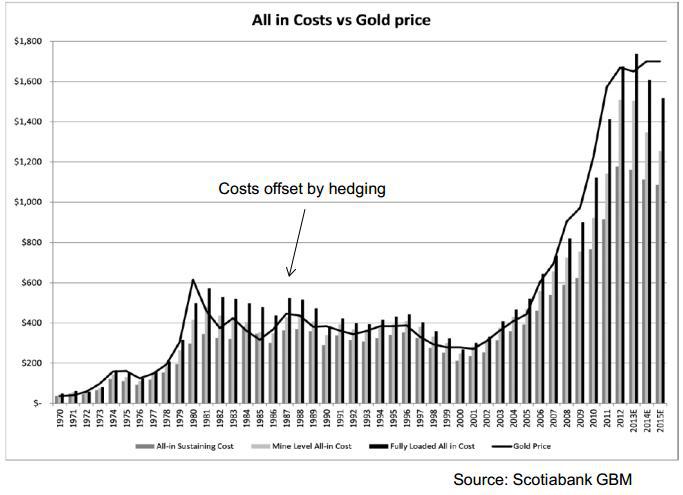

In June 2013, the World Gold Council (WGC) published a guidance note on the all-in sustaining cash cost metric for gold mining companies. This way, investors can have a better evaluation on the real cost of mining gold. This metric adds additional costs which reflect the varying costs of producing gold over the life-cycle of a mine. To name a few: by-product cash costs, sustaining capital, corporate general and administrative expenses, and exploration costs. We calculate all-in sustaining costs as the sum of total cash costs (net of byproduct credits), sustaining capital expense, corporate, general and administrative expense (net of stock option expense) and exploration expense.

There is one flaw in this system though. These all-in costs only include additional all-in sustaining costs and do not include CAPEX for projects. If we would include these project costs, we would get an astounding $1784/ounce in 2012 for the bigger gold mining companies. Nevertheless, it’s a first step in the right direction.

It is interesting to analyze how the all-in sustaining cash costs have progressed in 2013 as compared to 2012. All-in cost data has been taken from a research report of Dundee Capital Markets for the 2012 estimate.

|

| Chart 1: All-in costs gold miners 2012 (Dundee Securities) |

We see here that many gold miners are producing just under the average gold price of $1600/ounce in 2012.

Now we fast-forward to 2013, take data from a recent Denver Gold luncheon for the 2013 AISC cost estimate.

|

| Chart 2: AISC gold miners 2013 (Agnico Eagle) |

Again we see that the all-in sustaining costs are hanging just below the current average gold price of $1300/ounce in 2013.

Now let’s compare these numbers year over year. Read on here.