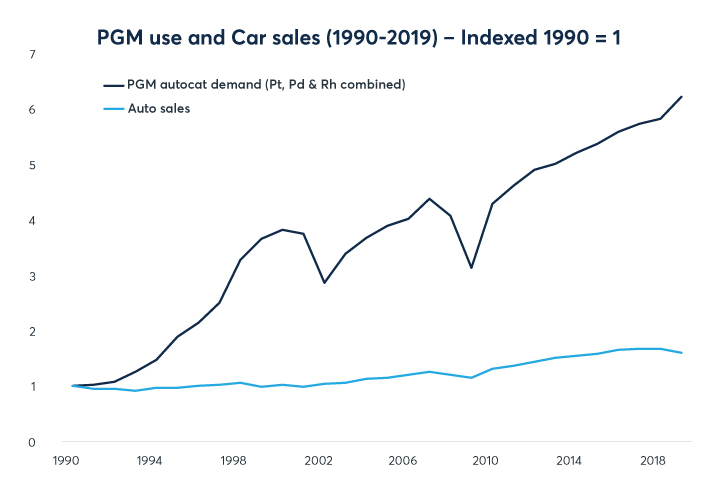

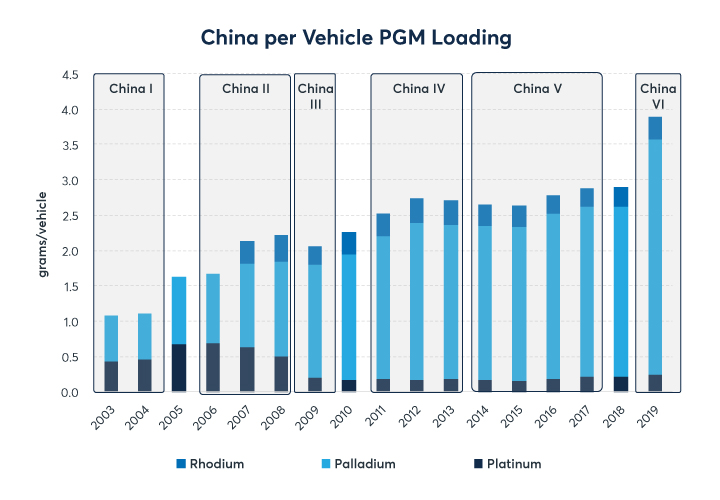

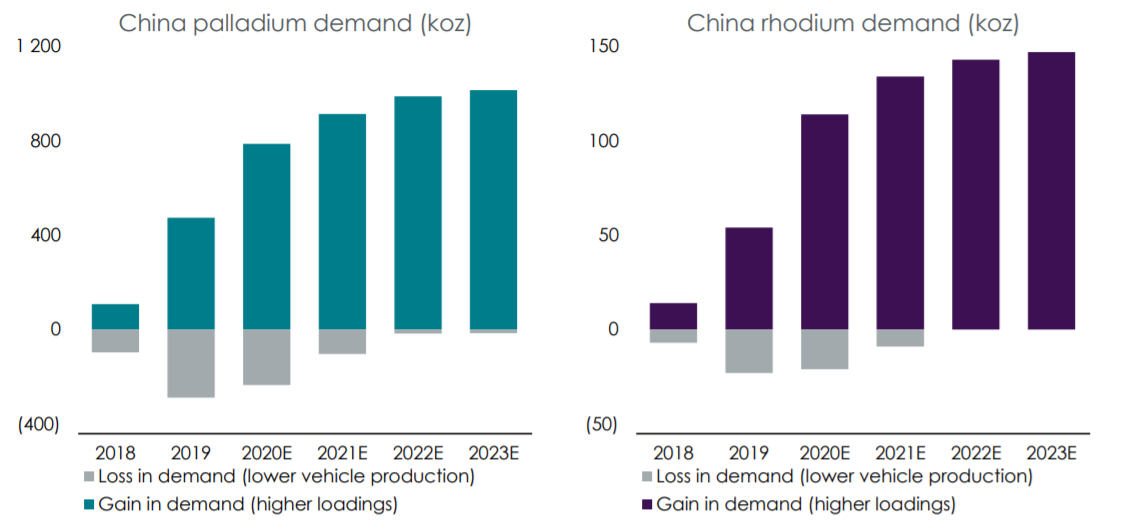

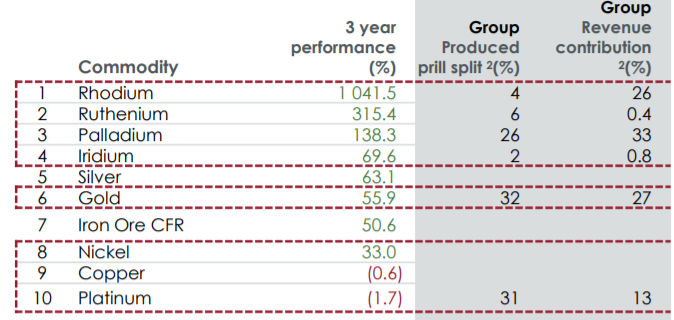

Vehicles need autocatalysts like rhodium/palladium/platinum. China is increasingly using more of these PGM’s in their vehicles.

Vehicles need autocatalysts like rhodium/palladium/platinum. China is increasingly using more of these PGM’s in their vehicles.

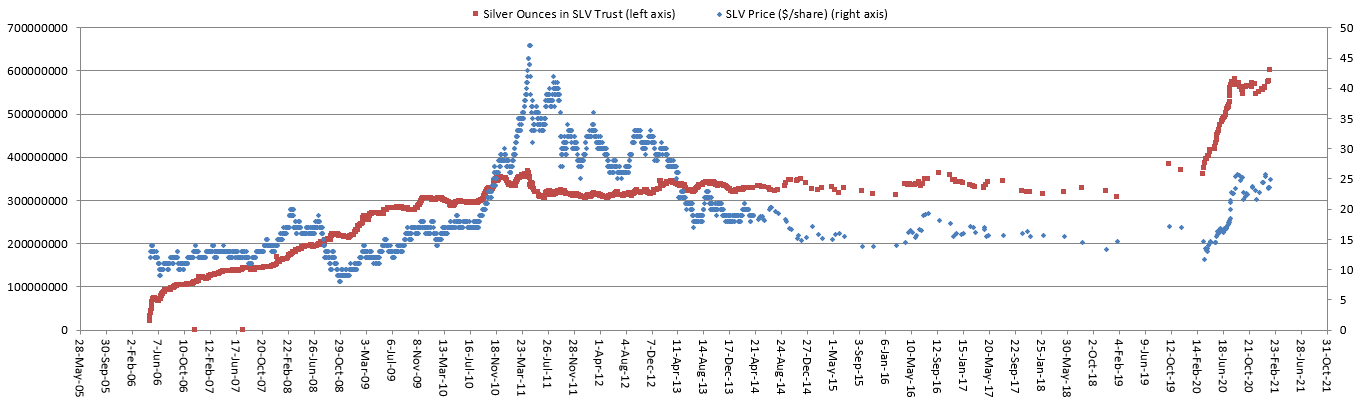

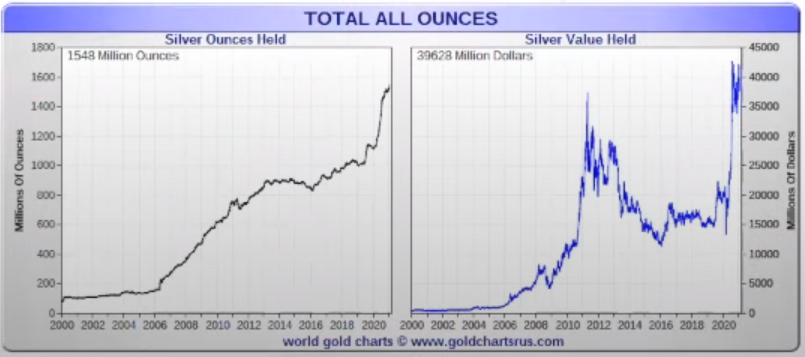

Wallstreetbets has ignited a buying frenzy in the SLV trust pushing the amount of ounces in the trust to a record high.

The silver price should be going up together with the amount of physical silver ounces held.

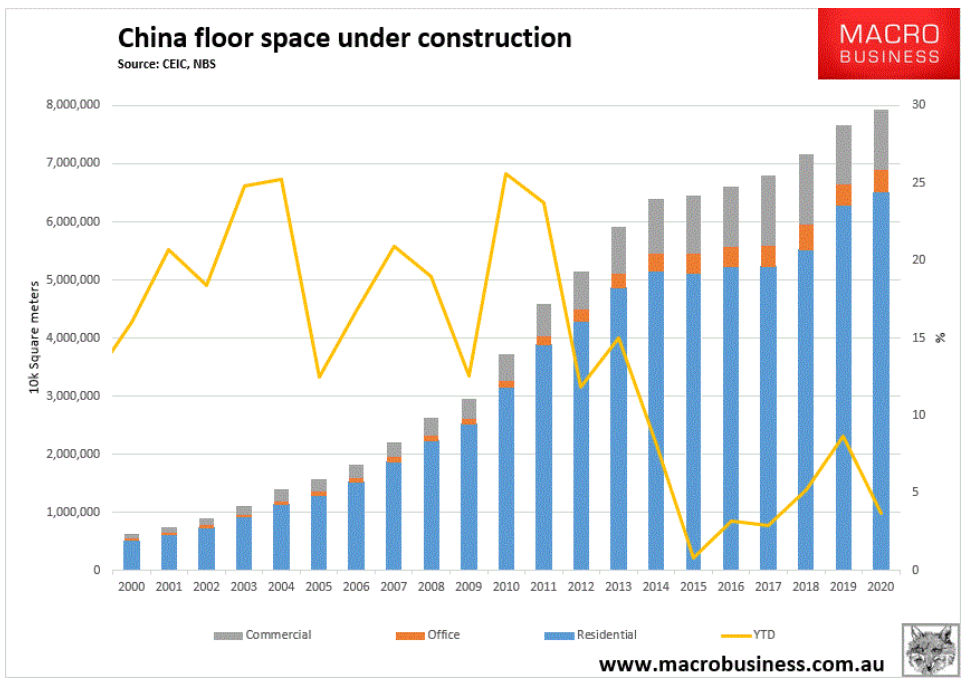

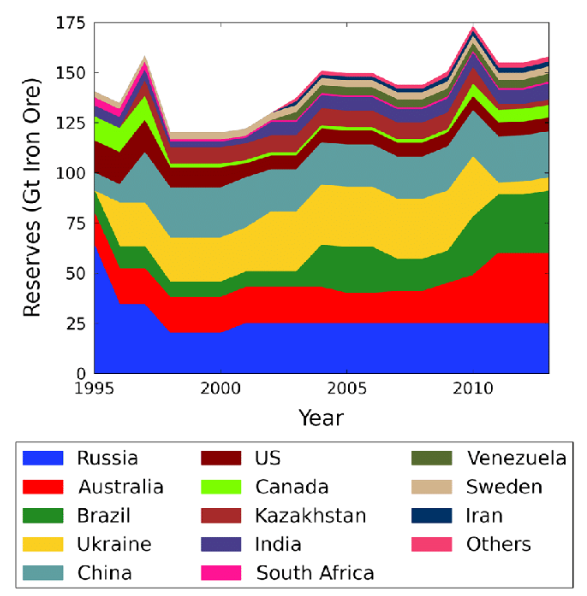

Iron ore is correlated to China construction.

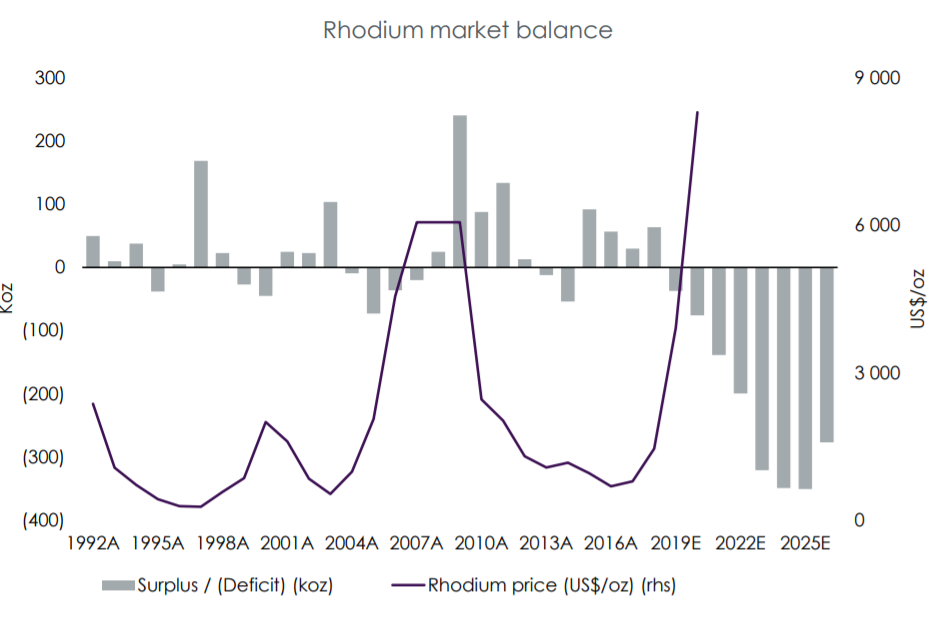

Platinum, palladium and rhodium have all been moving higher and I expect them to go higher as China is loading more palladium and rhodium in their vehicles. China vehicle sales have rebounded as well.

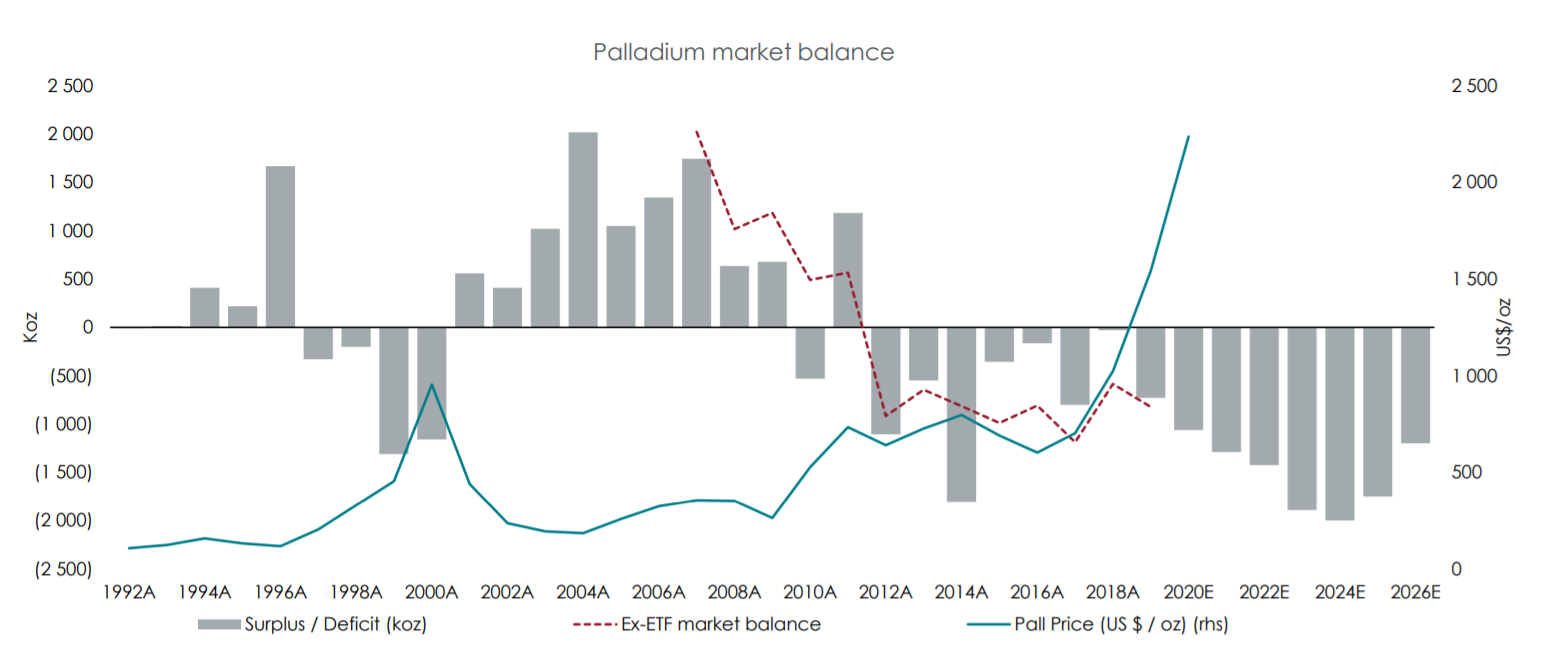

Platinum is going to be used in 3-way catalysts, which will boost platinum prices. Sibanye-Stillwater expects platinum to reach $2000 per ounce in 2025.

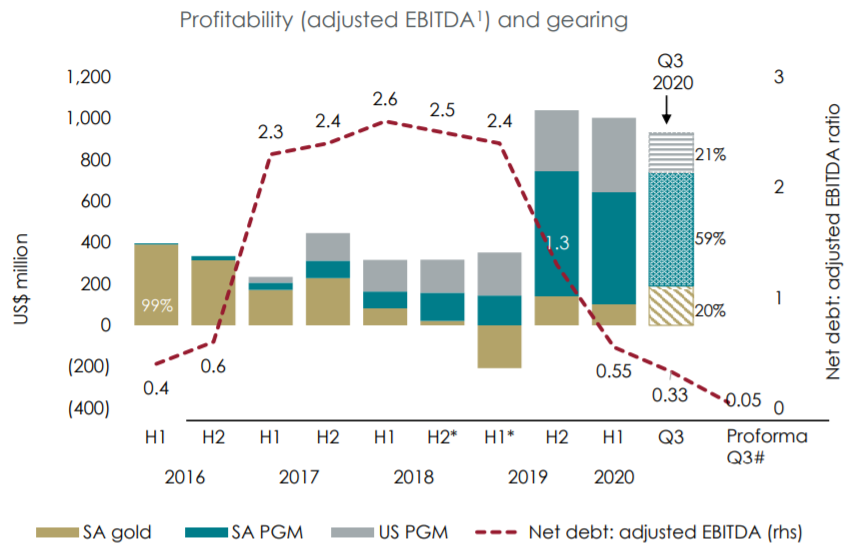

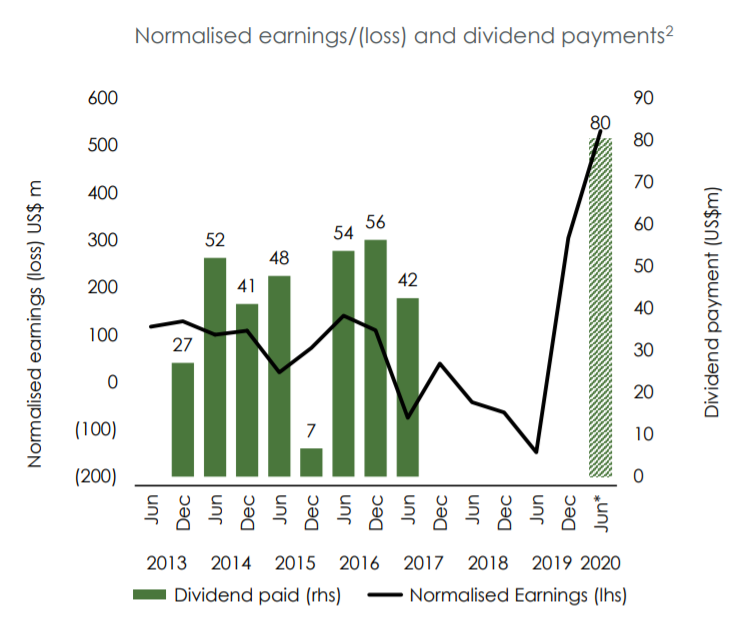

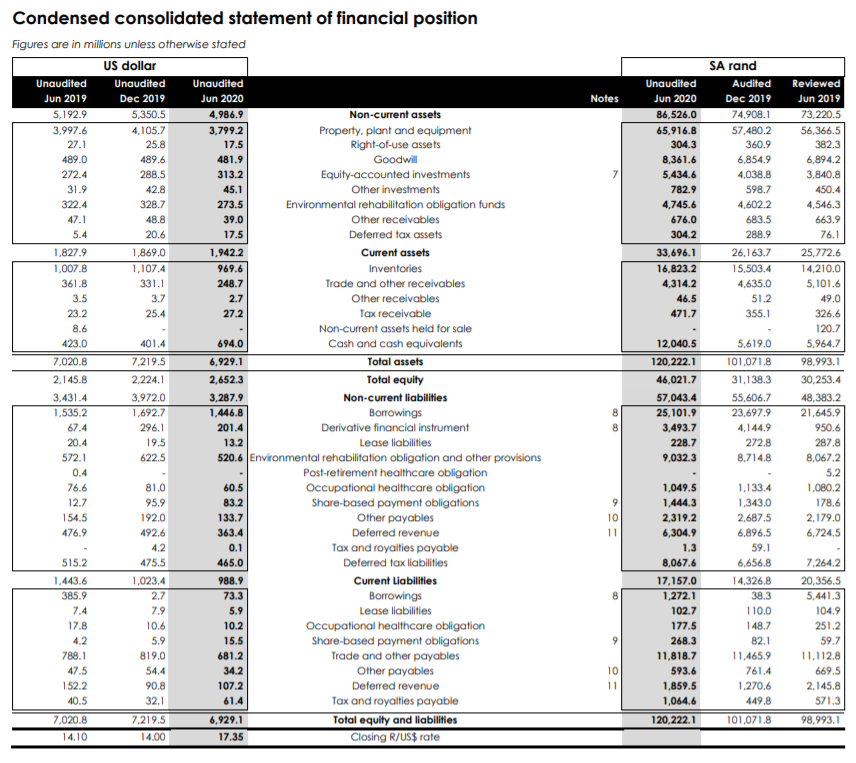

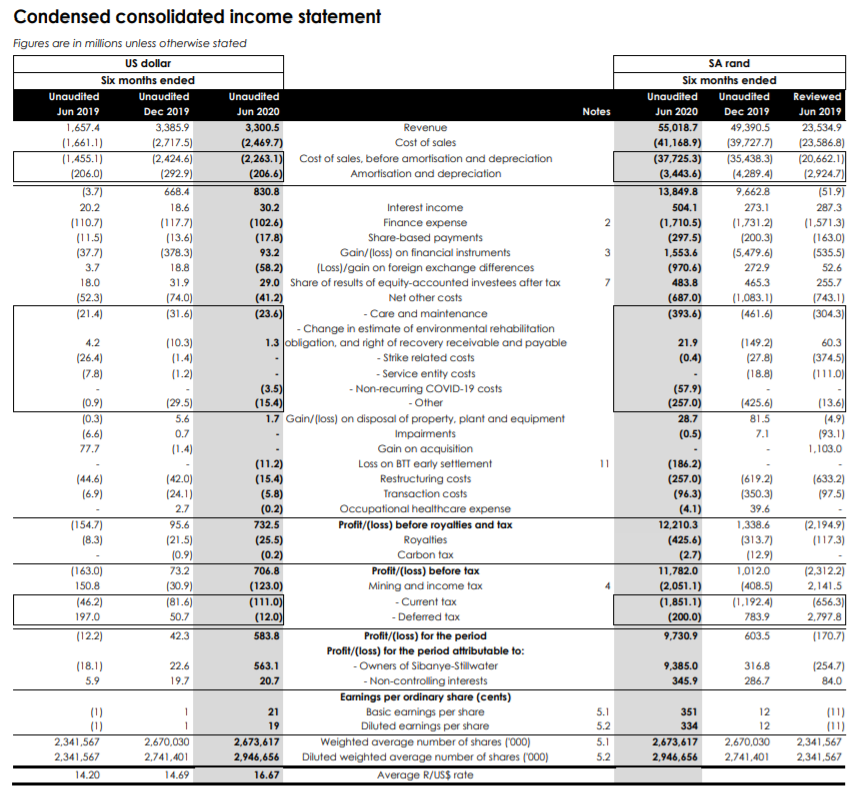

SBSW’s EBITDA was $922 million in Q3 2020. This translates to $3.7 billion EBITDA per year. With a 5 multiple, SBSW should be valued at $18 billion market cap. So there is 50% upside. The company has no net debt.

Net earnings were $1 billion per year in 2020, but is expected to rise 66% on higher rhodium/platinum prices and higher production numbers. Earnings per share are expected to be at $3.52 per share, which gives Sibanye-Stillwater a P/E of 4.8 which is very cheap.

On top of this, SBSW is expected to offer a dividend yield of 8% and is also moving into the battery metal space.

But price to earnings ratio is ok at 5-7.

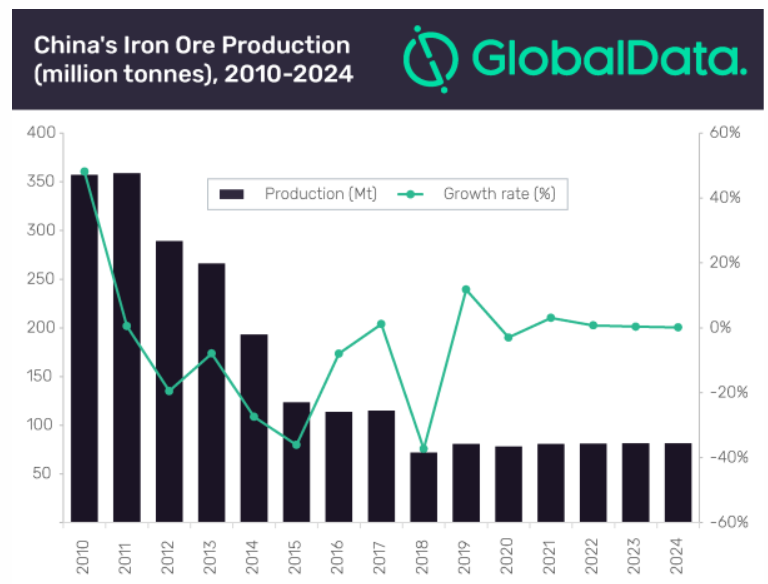

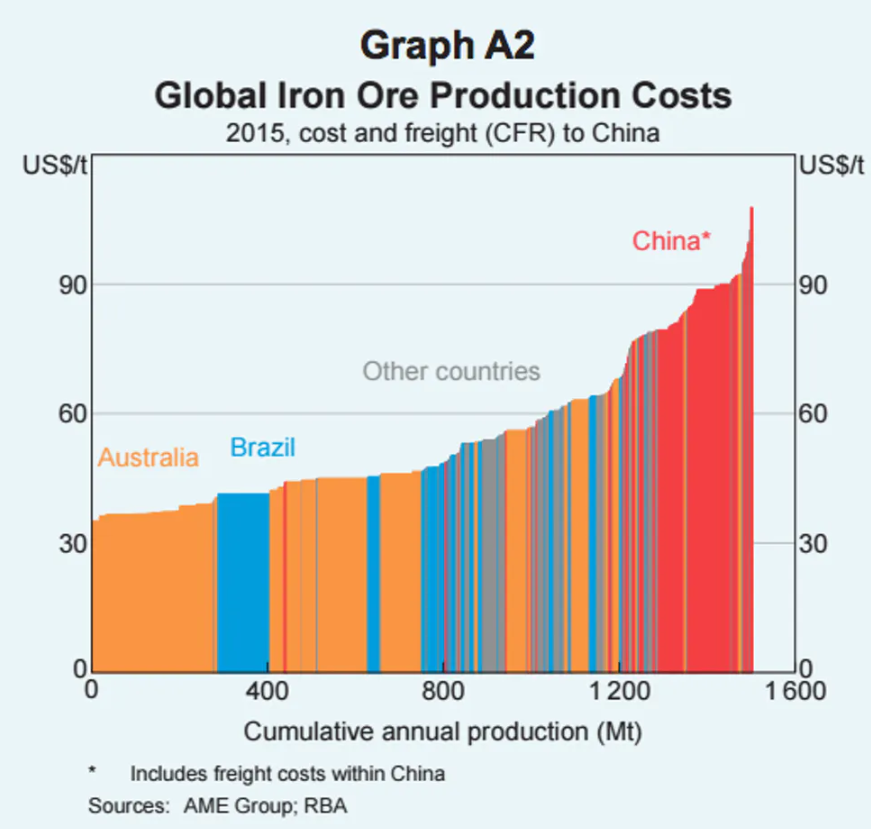

China’s iron ore production is not growing.

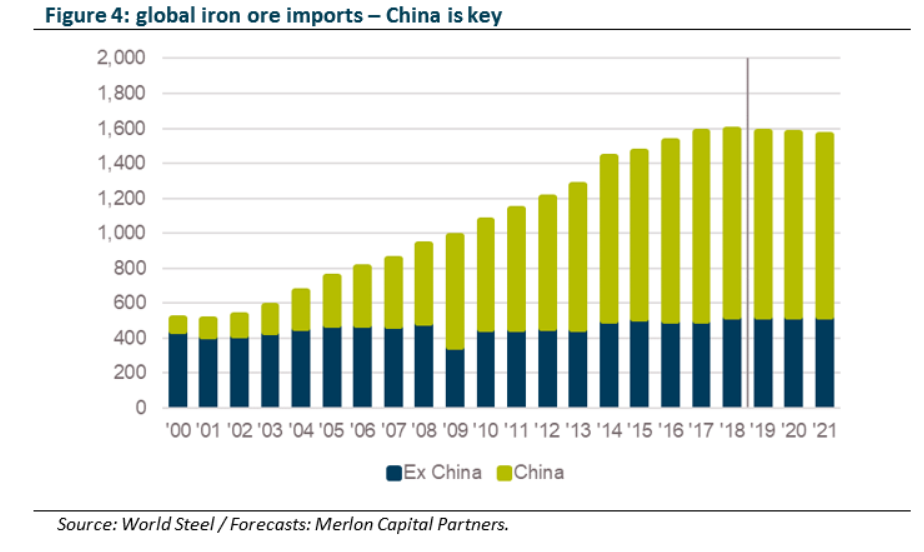

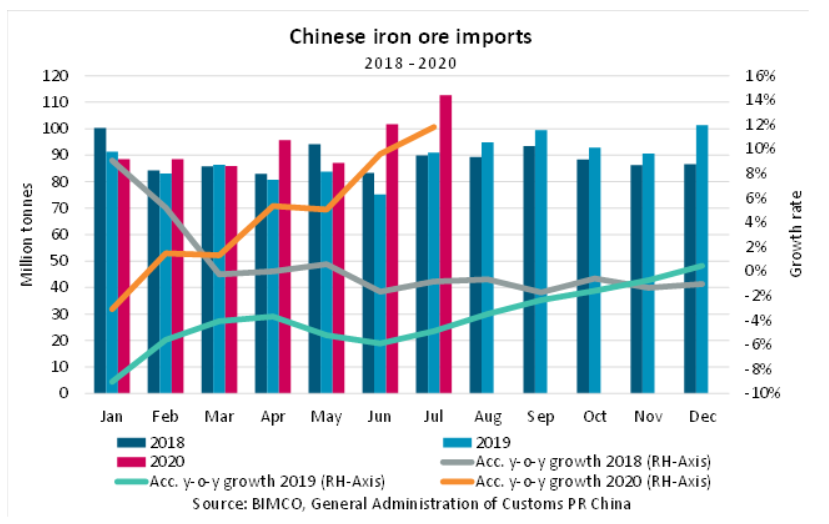

China is the largest iron ore consumer and iron ore imports are growing.

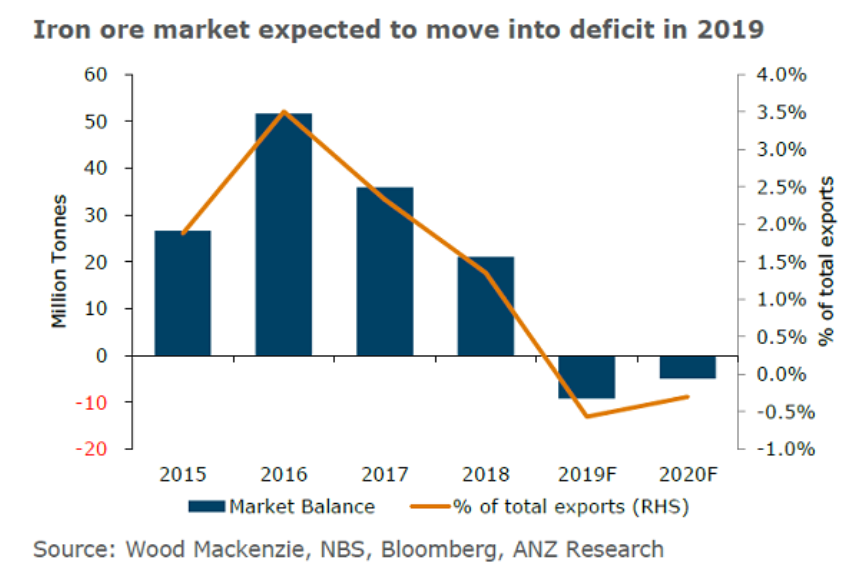

Iron ore is currently in deficit.

Therefore Vale is a good investment.

Commodities should be bought during seasonally strong periods.

Industrial metal price seasonality

Copper

Zinc

Aluminium

Iron ore

Precious metal price seasonality

Gold

Silver

Soybeans

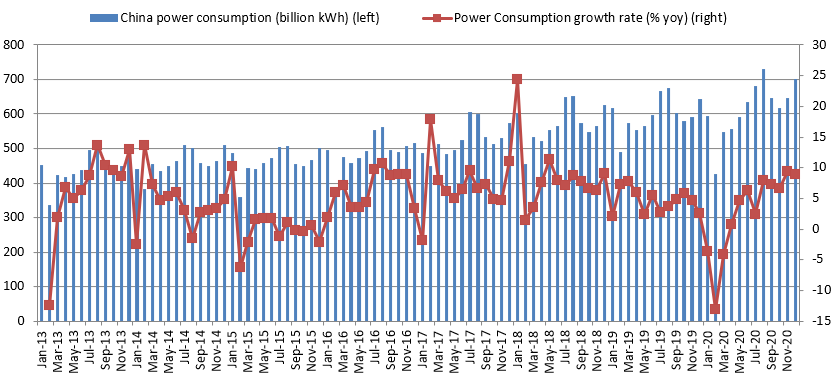

China power consumption hit a high of 8.8% in December 2020.

According to Sibanye, platinum will reach $2000/ounce in 5 years.