There is all this talk about “tapering”. Will the Federal Reserve taper or not taper, that’s the question. To find the answer, we need to take a look at the U.S. national debt.

This is really a weird sight, do we really have an actual debt ceiling? Aren’t we going to raise the debt ceiling? U.S. public debt has been growing at almost $200 billion a month and has been staying flat just recently.

|

| Chart 1: U.S. Public Debt |

Since May 19, 2013, the debt ceiling has been stuck at $16.735 trillion and this ceiling has been in place for almost 2 months as chart 1 suggests. The treasury says that they would be able to pay all the bills until October by enacting extraordinary measures from May 20 till August 2.

In all, the Treasury has the following measures available to it:

- Suspend the investments of the Thrift Savings Plan G Fund (otherwise rolled over or reinvested daily, such investments totaled $130 billion in Treasury securities as of May 31, 2013);

- Suspend investments of the Exchange Stabilization Fund (otherwise rolled over daily, such investments totaled $23 billion as of May 31, 2013);

- Suspend the issuance of new securities to the Civil Service Retirement and Disability Fund and Postal Service Retiree Health Benefits Fund (totaling an estimated $79 billion on June 30, 2013, and about $2 billion each subsequent month);

- Redeem early securities held by the Civil Service Retirement and Disability Fund and the Postal Service Retiree Health Benefits Fund equal in value to expected benefit payments (valued at about $6 billion per month);

- Suspend the issuance of new State and Local Government Series (SLGS) securities and savings bonds (between $4 billion and $17 billion in SLGS securities and less than $1 billion in savings bonds are issued each month); and

- Replace Treasury securities subject to the debt limit with debt issued by the Federal Financing Bank, which is not subject to the limit (up to $8 billion).

And due to higher tax revenues at the start of 2013, we see that interest payments on government debt weren’t a problem. In fact, the interest payments as a percentage of tax revenue has been declining since 2013 (Chart 2).

|

| Chart 2: Interest payments as a % of tax revenue |

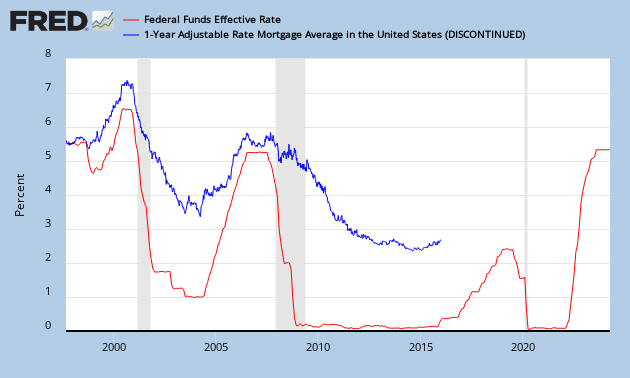

Though, there is one parameter that was not anticipated and that is the effect of higher interest rates and higher mortgage rates.

Read the analysis here.