In this post I will try to explain how important it is to watch the total marginal cash cost of gold mining to predict where the gold price (GLD) will be headed to. This marginal cost can be divided in two parts: cash cost of production and other costs (exploration, construction, maintenance, etc…) and stands at around $1300/ounce. With the recent decline in the price of gold, I believe we have finally hit the bottom.

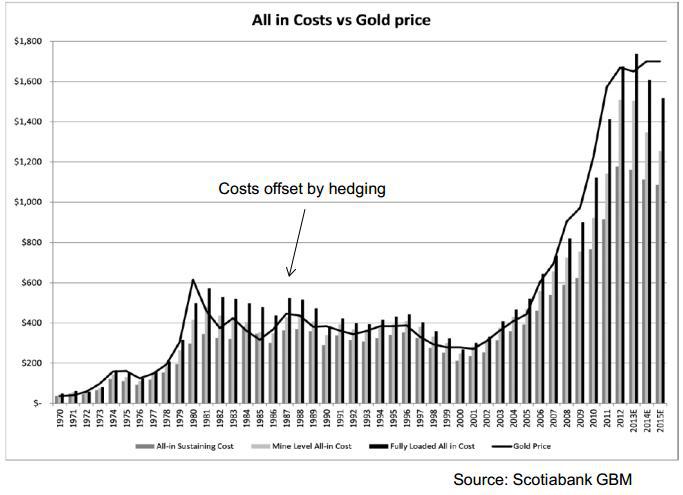

The gold price has always followed the marginal cost of suppliers throughout history (Figure 1). The correlation between gold prices and gold mining cash costs between 1980 and 2010 stood at 0.85, which is pretty highly correlated (Source: CPM Gold Yearbook 2011).

With the price of gold at $1400/ounce today I’m pretty sure we can’t go much lower if this correlation proves to be correct.

The following chart is the most important chart every gold investor needs to be aware of. As I mentioned before, there is a high correlation between the all in cash costs of gold mining and the gold price (Chart 4). So investors need to monitor the total cash cost of gold mining in order to predict the trend in the gold price itself.

|

(click to enlarge)

|

Continue reading here.